|

💡 Tip of the Week

If your income is unpredictable, stop using your bank balance as your “plan.” Build a buffer/system that separates inconsistent deposits from consistent expenses.

|

In This Issue

|

1

|

The real problem: timing, not revenue

|

› |

|

2

|

The Drip Account Method: smooth cash flow fast

|

› |

|

3

|

How this applies beyond the healthcare industry

|

› |

|

Presented by

|

|

|

QuickBooks Cleanup Sprint — Fast Path to Clarity

Turn messy books into decision-ready numbers fast—then we teach you how to keep them clean and cash-smart going forward.

|

✓

Save on tax filing by providing clean financial statements

|

|

✓

Streamlined bookkeeping so you can see where cash is going

|

|

✓

Owner training on what to watch monthly

|

|

✓

Someone in your corner who actually cares

|

Clean books, clear choices.

|

|

|

|

|

Cash Flow Roller Coaster? Fix the Timing, Not the Revenue

|

|

|

|

Watch this edition instead

How to smooth your cash flow so slow weeks don't feel so stressful

|

Play Video →

|

|

|

|

One of our chiropractic clients bills mostly insurance, and for years cash flow felt like a weekly coin toss.

He could have a “great week” clinically, full schedule, strong production, and still open his bank app on Friday and feel his stomach drop.

Because the deposits didn’t match the work.

Some weeks insurance paid fast and everything felt easy. Other weeks claims lagged, got denied, or bounced back for resubmission, and suddenly payroll was due, rent was due, vendors were due, and he was doing the mental math we all hate:

“If this deposit doesn’t hit by Tuesday, what gets delayed?”

Here’s what mattered most: his practice wasn’t failing. Revenue was there.

The real problem was the timing, money coming in on insurance’s schedule, while expenses came out on a very predictable schedule.

Once we named it for what it was, a timing problem, the fix became much simpler.

The breakthrough wasn’t “more patients.” It was building a system that smooths the swings so low deposit weeks stop feeling like emergencies.

If your business doesn't deal with insurance, keep reading. Every business in every industry experiences revenue fluctuations. THe principles below can help reduce the stress you feel whenever there's more bills than money.

|

Why this feels so stressful

The real issue is simple:

collections come in on insurance timing, while your expenses run on a fixed timeline.

If you don’t build a system in the middle, the business will always feel like it’s yanking you around.

You end up checking the bank balance like it’s a weather forecast, hoping this is the week everything lines up.

That’s not a system, that’s survival mode.

|

The hidden cost of “inconsistent weeks”

- You hesitate to hire or invest, even when the practice is doing well.

- Big deposit weeks create false confidence, and spending creeps up.

- Slow weeks feel like emergencies, even when the business is healthy.

- You carry the stress home because the uncertainty never shuts off.

|

You didn’t build a business to obsess over cash flow every week. You built it to help people and provide for your life and family.

|

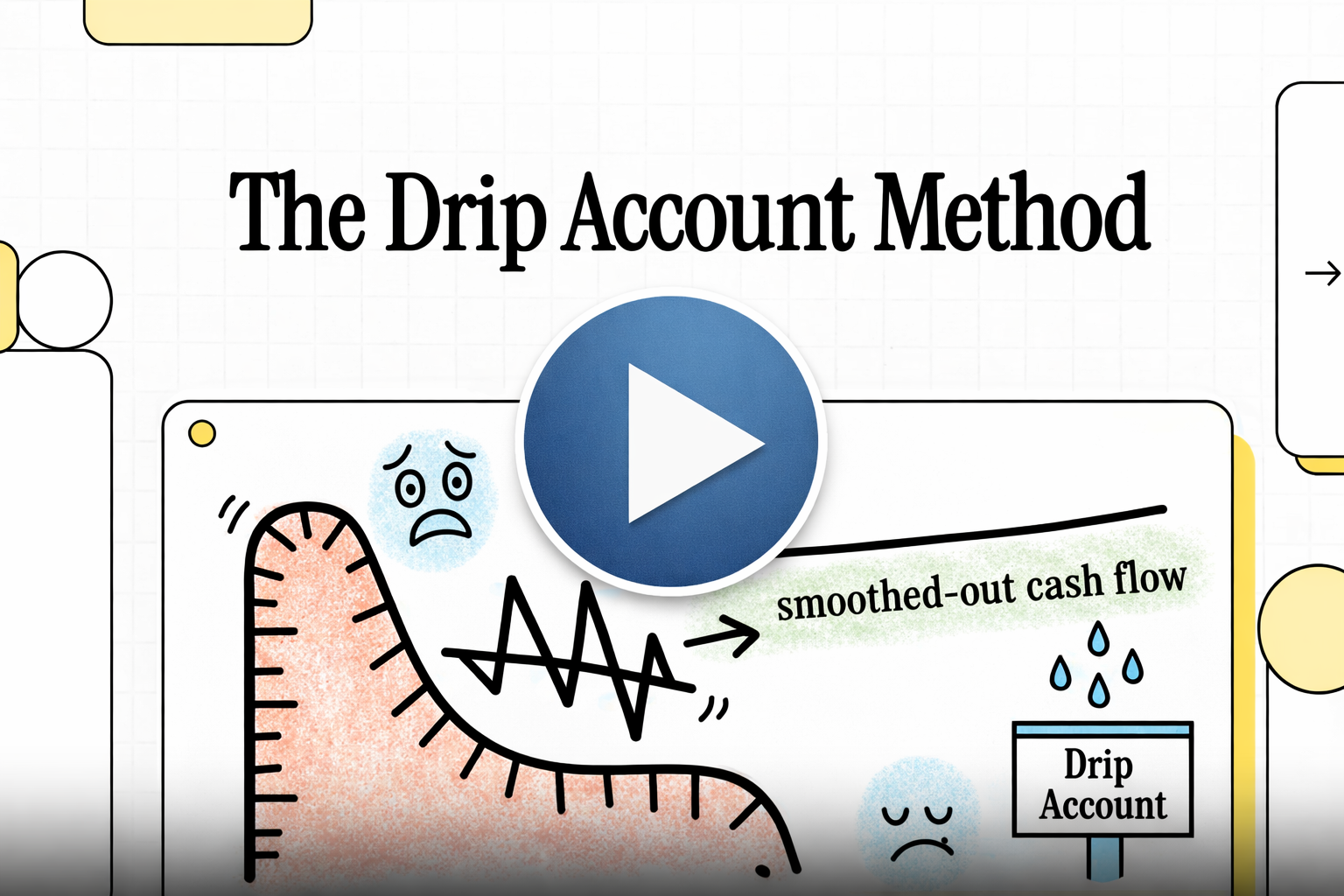

The Drip Account Method (cash flow smoothing)

What saves owners with seasonal or unpredictable income is a simple concept:

create a buffer between inconsistent revenue and consistent expenses.

We call it the Drip Account Method.

It helps level out cash flow so you can cover expenses, pay yourself, and stop letting collections control you.

|

Step 1: Find your weekly “nut” (or "monthly nut" if you're business runs on more of a monthly schedule)

Run a Profit and Loss report for the last 12 months. Take total expenses (payroll, rent, software, supplies, everything).

If owner pay isn’t included, add what you pay yourself (or should pay yourself).

Divide by 52 (or 12 for the monthly nut). That’s your baseline. It’s the number that makes the business feel “normal” week to week.

|

|

Step 2: Open one new bank account

Not a spreadsheet line. An actual account.

Name it “Drip” (or “Timing Reserve”).

This becomes your cash smoothing buffer. Extra money goes there in strong weeks and drips back in during slow weeks.

|

|

Step 3: Follow one weekly rule

- If cash deposits are above your weekly nut, move the extra into the Drip account.

- If cash deposits are below your weekly nut, move the difference back into operations.

|

That’s it.

You’re not guessing which insurance claims or customers will pay. You’re creating a buffer between inconsistency and reality.

Slow weeks stop feeling like emergencies. Big deposits stop messing with your judgment. The business starts to feel steady.

|

How this applies beyond healthcare

Even if you don’t bill insurance, the timing problem shows up anytime revenue is seasonal, project-based, or unpredictable.

The principle is the same: separate lumpy income from steady expenses.

|

Quick examples

- Contractors: deposits come in bursts, but payroll and materials run weekly.

- Med spas / aesthetics: busy seasons spike cash, slow seasons test discipline.

- Dental practices: production can be stable, collections can be lumpy (insurance + financing).

- Fitness studios: membership waves and promotion cycles create uneven deposits. Prepayments front-load cash while expenses come over time/

- Home services: weather swings and cancellations create unpredictable or dead months, especially in winter.

- E-commerce: launch weeks and ad cycles spike revenue, then drop back down.

|

If any of these sound like you, test the Drip Method for 30 days. The goal isn’t perfection. It’s stability, clarity, and less stress.

|

Want help setting it up?

I put together a free resource called the Drip Account Cash Flow Planner. It helps you pull the numbers, figure out your weekly nut, and know exactly what should stay in operations versus what should move into the drip account.

Reply to this email and tell me:

“Send me the Drip planner”

and I’ll get it to you.

You deserve a business that feels steady, not one that yanks you around.

|

Bottom Line

|

If cash feels inconsistent, it’s usually timing.

Build a buffer that smooths deposits into a steady plan, and the stress drops fast.

|

|

|

SCHEDULE A STRATEGY SESSION NOW!

Adam Litster

Chief Profit Architect

(816) 500-5779

[email protected]

www.betterbizinfo.com

Simple systems. Consistent profit.

|

How do you like this edition of The Profit Shift?

|

Framework Summary

|

V

VISIBILITY

Learn the power of accurate information

|

|

|

P

PROFITABILITY

Grow your cash using disciplined expense control

|

|

|

S

SCALABILITY

Create a market-dominating position through your powerful offer

|

|

|

|

Free Sweet Spot Assessment

Find the work you do best, the clients who value it most, and the offers that scale. Take the quick assessment for personalized recommendations and a clear next-step plan.

|

|

|